GRI standards – what is the fuzz about?

Introduction

Many sustainability-related topics, phrases, and abbreviations emerged due to the increasing awareness of climate urgency. One of them is GRI, which stands for the Global Reporting Initiative. This article aims to give a brief overview of GRI and its Standards and explain its popularity.

As mentioned, human impact on the natural environment is becoming impossible to ignore, while COVID-19 has reversed many years’ worth of social improvements across the planet. These have contributed to the ever-growing attention to societies´ sustainability efforts from the public´s and regulators´ points of view.

Businesses are increasingly being held accountable for their impacts and are expected to provide full transparency in acknowledging and managing those impacts. This is where various frameworks and standards come into play, as they support disclosing non-financial, i.e., sustainability-related information in a comparable and uniform way. It may not come as a surprise that a wide array of such structures are in place (many of them indicated below), all somewhat different in their approach, target sector, level of detail, scope, etc.

The story of GRI

One such standard is developed by a Global Reporting Initiative (GRI) called GRI Standards. GRI Standards were first launched in 2000 (then called GRI Guidelines). Since then, “the world’s first globally accepted standards for sustainability reporting” have received continuous evaluation and improvement in time and become the world leader among voluntary performance reporting programs.

In 2020, 73% of the world´s 250 largest companies by revenue reported their non-financial information following the GRI Standards. Closer to home, companies using GRI Standards include Tele2, Stora Enso, Maxima, and AS Tallinna Vesi, to name a few.

Ever since the foundation of GRI, there have been two principal goals for the guidelines:

- To harmonise, clarify and unify non-financial reporting and

- To empower societal actors to demand a certain level of accountability from the companies through access to information and the use of market mechanisms.

GRI Standards are issued by the Global Sustainability Standards Board (GSSB), an independent multi-stakeholder standard-setting body established by GRI. It ensures that the Standards are developed independently and in the public interest. To involve the considerations of different perspectives, the GRI Standards are developed by Expert Working Groups representing various stakeholder groups such as civil society, business enterprises, labour organisations, etc.

Before issuing any new GRI Standard, its draft is released for public comment. It is precisely this thorough multistakeholder inclusion that has accompanied the Standards´ development since its beginning that has contributed to their completeness and facilitated dialogues across different participants of the society.

The framework of GRI standards

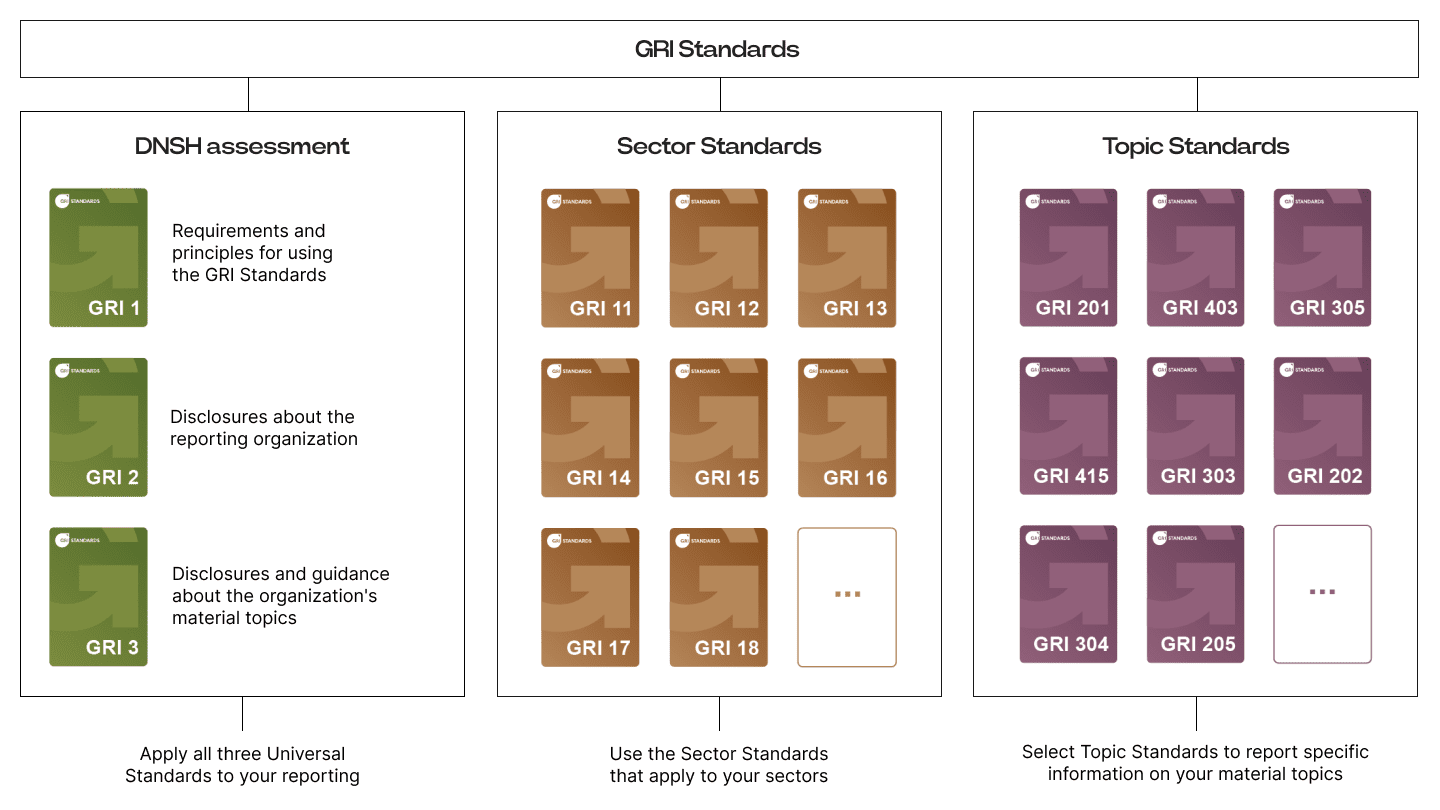

Having looked into the past, a brief overview of the GRI Standards is due. The Standards have a modular structure consisting of Universal -, Sector -, and Topic Standards, all freely accessible from the GRI website.

Universal Standards apply to all who wish to report following GRI Standards as they give an introduction to the Standards (GRI 1), list general disclosures for the reporting organisation (GRI 2), and describe the selection process for material topics (GRI 3). “Material topic” is one of the central concepts of GRI Standards and stands for “topics that represent the organisation’s most significant impacts on the economy, environment, and people“, thus covering the most important ESG (Environment, Social, Governance) impacts.

Only after identifying the material topics (using GRI 3: Material Topics 2021) can the reporting organisation proceed with the Topic Standards. This module consists of separate standards – for example, „GRI 207: Tax 2019“, „GRI 302: Energy 2016“, and „GRI 401: Employment 2016“ – each containing disclosures relevant to the given topic. The organisation must report only those disclosures that represent impacts related to its material issues.

Sector Standards list the topics likely to be material for an organisation within the given sector. Currently, three sector standards have been published: a) the oil and gas sector, b) the coal sector and c) the agriculture, aquaculture and fishing sectors. Companies must use an applicable Sector Standard when available but still need to identify its material topics.

The modular structure of GRI Standards enables an easier update of its individual parts and facilitates an easier understanding of the entire system. Furthermore, by having a separate standard for each topic, the reporting is supported by thorough context-specific recommendations and guidelines.

GRI standards support other disclosure frameworks

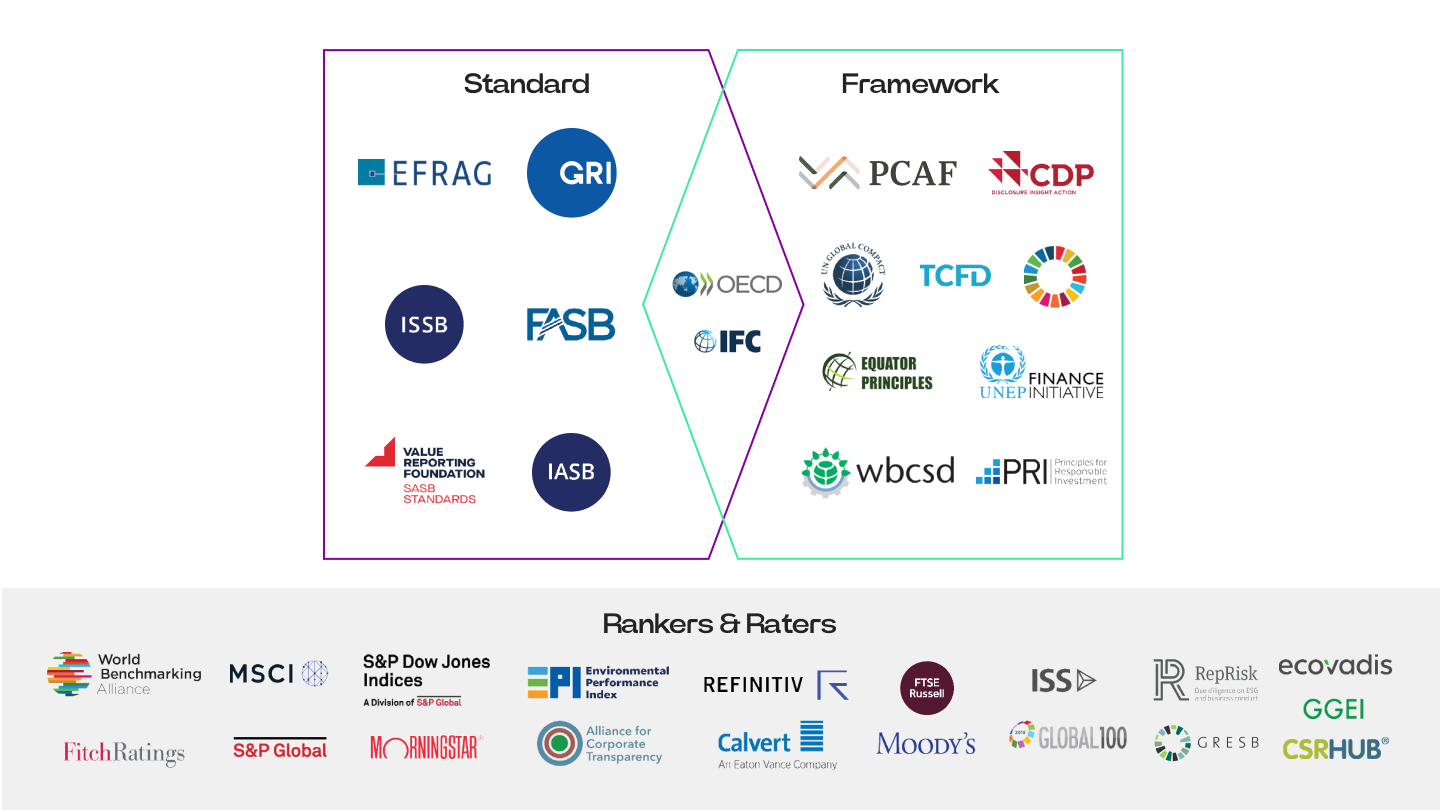

Acknowledging the different information needs of various stakeholders and wishing to extend its vision of uniformity beyond GRI Standards, GRI has collaborated with other sustainability disclosure frameworks and developed guidelines on how to use its standards together with other related initiatives.

The examples include: “A Practical Guide to Sustainability Reporting Using GRI and SASB Standards” and “Linking GRI and CDP”. Such alignments enable organisations to follow multiple disclosure systems while keeping additional efforts at a minimum.

Furthermore, in March 2021, GRI and the European Financial Reporting Advisory Group (EFRAG) announced their cooperation wherein GRI pledged to participate in the construction of European Sustainability Reporting Standards (ESRS) to be used when reporting under the European Corporate Sustainability Reporting Directive (CSRD) (read more on CSRD and ESRS from our other article here).

GRI and ESRS alignment enables the thousands of European companies who already use GRI Standards to comply with ESRS more easily. Therefore, using GRI Standards also helps navigate the ever-evolving legislative landscape.

In summary, GRI Standards have proven that the systematic communication of sustainability performance across a wide range of sectors and contexts is possible. It is clear that GRI has significantly impacted the field of sustainability disclosures. It is exciting to see where the new developments take us. After all, sustainable development rests on accountability, which can only be enforced through transparency.

We will help you with implementing GRI standards in the reporting process

Contact us if you want to understand GRI better or need help with the implementation process.

Our GRI-certified sustainability team member Liisa Õunmaa ([email protected]) is here to support you on this journey.