From resilience to scale: what Ukraine’s startup ecosystem needs next

Client

EU4Innovation EastEcosystem overview

Ukraine’s startup ecosystem has done more than withstand the full-scale war – it has continued to create new companies, attract international attention, and contribute to the country’s economic resilience.The country is now home to an estimated 2,600 active startups (~18% founded after 2022), with a combined enterprise value of around €30 billion. It is associated with ten unicorns and one decacorn – Ukrainian-founded Grammarly, and has improved its position in the StartupBlink Global Startup Ecosystem Index from 50th globally in 2022 to 42nd in 2025.

At the same time, the next stage of ecosystem development will require more than resilience. Ukraine has built several important foundations for a startup-supportive environment, but the ecosystem still faces structural constraints that limit the ability of founders to move from idea to validation, investment, market entry, and scale.

A new study prepared by Civitta with the support from EU4Innovation East project (funded by the European Union, co-funded by the French Government, and implemented by Expertise France) assesses Ukraine’s startup ecosystem through the lens of the European Startup Nations Alliance (ESNA) and its Startup Nations Standards (SNS). The report was prepared for the Ministry of Digital Transformation of Ukraine and the Ukrainian Startup Fund.

While the initial scope centered on ESNA benchmarking, the team went further and produced a comprehensive analysis of the Ukrainian startup ecosystem across five dimensions: governance and regulation, access to funding, access to talent, support infrastructure, and access to markets. The research combined desk analysis with a survey of 110 Ukrainian startups, 11 key informant interviews, and three thematic focus groups, capturing the practical conditions experienced by founders, investors, universities, support organizations, and public institutions.

What ESNA shows about Ukraine’s startup policy environment

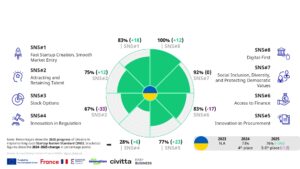

ESNA provides a common European framework for assessing how supportive national policy environments are for startup creation and growth. Its eight Startup Nations Standards cover areas such as fast company creation, talent attraction, employee stock options, innovation-friendly regulation, public procurement, access to finance, inclusion, and digital-first government.

Ukraine entered the scoreboard in 2024 with a strong debut: 4th place out of 24 participating countries, with an overall implementation score of 73% against an ESNA average of 61%. This performance placed Ukraine in the upper tier of European startup-policy environments, despite the difficult operating context created by full-scale war, macroeconomic pressure, and large-scale population displacement.

The first assessment recognized full implementation in stock options and access to finance, reflecting the Diia. City framework and the role of the Ukrainian Startup Fund, alongside high scores in social inclusion and digital-first government. Ukraine performed weakest in innovation in regulation, innovation in procurement, and fast startup creation.

The 2025 edition shows continued progress in a faster-moving field. Ukraine’s score rose to 76%, supported by gains in fast startup creation (83%, up 18 percentage points), innovation in procurement (77%, up 23 points), and a 100% in digital-first government, where Diia remains a European reference point. At the same time, Ukraine’s position shifted to 5th–6th place as the ESNA average rose from 61% to 70%, reflecting accelerating reform efforts across participating countries. The 2025 assessment also recorded lower scores in two previously full-mark standards, stock options and access to finance, while innovation in regulation remains the area with the most room for improvement at 28%, against an EU average of 55%.

Two takeaways follow:

- First, Ukraine remains in the upper tier of European startup-policy environments, but maintaining that standing will require continued reform momentum as other countries advance.

- Second, ESNA measures the maturity of policy frameworks, not the performance of an ecosystem. A strong formal score does not automatically mean that startups experience a seamless growth environment, and the study’s fieldwork shows the practical picture is more mixed.

Strong digital foundations, but fragmented startup policy

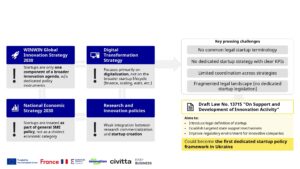

Ukraine’s digital public administration is one of the country’s clearest ecosystem strengths. Through Diia, Diia.City, Diia.Business, and related digital transformation initiatives, the state has reduced administrative friction and made many interactions with public institutions faster and easier. For founders, this creates a real advantage, especially in areas such as business registration and access to digital services. Yet digitalisation alone does not create a complete startup policy system.

The report finds that Ukraine still lacks a coherent startup-specific governance framework. There is no fully established legal definition of a startup or scale-up, no systematic startup impact screening in regulatory processes, and no unified ecosystem data infrastructure that would allow public institutions to track startup development consistently across sectors, regions, and stages.

As a result, startup-relevant initiatives often operate as separate instruments rather than as parts of a connected system. Institutions such as the Ukrainian Startup Fund, BRAVE1, GovTech Lab UA, Diia.Business, university initiatives, and regional support actors all play important roles, but the links between them remain uneven.

The practical consequence is that founders can encounter a highly modern digital interface in one part of the system and much more traditional, less startup-adapted procedures in another. This is especially visible in regulation, technology transfer, foreign-founder onboarding, investment structuring, and public procurement.

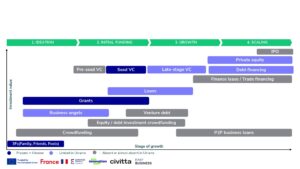

Access to finance remains the main bottleneck

Ukraine’s access-to-finance score under ESNA is formally strong, but the report shows that the practical financing ladder remains incomplete.

Investment activity has significantly recovered after the sharp decline in 2022, with disclosed tech investment reaching close to $500 million in 2025, against a wartime low of $209 million in 2023. Grant funding grew 11-fold over the same period, from $7 million in 2023 to $78 million in 2025. But $60 million of that 2025 grant volume went to defense tech through BRAVE1, leaving $18 million for the entire civilian segment. These are important signs of ecosystem activity and investor confidence in selected sectors.

However, the financing landscape remains narrow and uneven across startup stages. Many early-stage startups still rely heavily on bootstrapping, while pre-seed funding is limited, angel investment remains volatile and under-institutionalised, and later-stage domestic capital is scarce. Alternative financing instruments such as venture debt, investment crowdfunding, peer-to-peer business lending, and IPO pathways are either underdeveloped or not functioning as meaningful options for most startups.

A further structural issue is that a large share of investment is executed through foreign jurisdictions. This reflects investor preferences, legal and corporate governance constraints, and the absence of a mature local capital markets infrastructure. In practice, many Ukrainian-founded startups still need to move their investment structures abroad to become investable at later stages.

The report therefore argues that access to finance should be treated not simply as a shortage of money, but as a financing-pathway problem. Ukraine needs a more coherent funding ladder in which public and donor resources support the stages where market capital is weakest, while also helping crowd in private investors.

Key priorities include restoring a stable civilian early-stage funding anchor, developing matching grants and co-investment mechanisms, strengthening the business angel base, and expanding alternative financing channels adapted to startup realities.

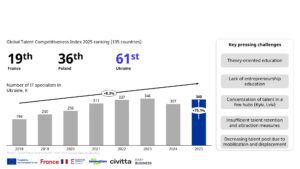

Ukraine has strong talent, but needs stronger talent conversion

Talent remains one of Ukraine’s most important startup assets – Ukraine’s IT workforce grew 75% between 2018 and 2025, reaching roughly 340,000 specialists, the second-fastest growth in Central and Eastern Europe. The country has a large and adaptable technical workforce, strong software engineering capacity, and a long-standing base of IT and outsourcing expertise. This gives startups access to product development capabilities that many ecosystems struggle to build.

But the issue is no longer only whether Ukraine has technical talent. The bigger question is whether that talent can be retained, upgraded, and converted into founders, early startup employees, commercially capable researchers, and scale-up managers.

The war has compressed the talent pool through displacement, emigration, mobilisation-related constraints, and long-term uncertainty, while education remains theory-heavy and disconnected from entrepreneurship.

The report highlights a clear talent-conversion challenge. Ukraine has technical capability, but too little of it is systematically transformed into startup teams, venture builders, product companies, or internationally scaling businesses.

Addressing this requires a stronger entrepreneurial culture, better integration of entrepreneurship education into universities, more practical exposure to startup environments, and clearer pathways from research and technical education into venture creation. It also requires a stronger international layer, including structured diaspora engagement, return-oriented programmes, and better conditions for attracting foreign specialists and founders.

Support infrastructure exists, but the pipeline is incomplete

On paper, the startup support in Ukraine’s landscape appears extensive: incubators, accelerators, hubs, university programmes, entrepreneurship centres, EDIHs, laboratories, prototyping spaces, and donor-funded initiatives.

In practice, the support system remains fragmented, unsustainable, and generalistic. Many initiatives are short-term, donor-dependent, concentrated in a few major hubs, or focused mainly on early-stage startups. Support for idea-stage teams, university spin-offs, and deep-tech ventures is still limited. Sectoral specialisation is also uneven, with defence tech standing out as the clearest exception. Programs targeting scaling or global expansion are essentially absent.

The hard infrastructure layer faces a related problem. Universities and research institutions often have equipment and laboratories, but these assets are not yet organised as accessible product-development infrastructure for startups. As a result, existing physical capacity is underused, especially by hardware, deep-tech, and engineering-intensive teams that need prototyping, testing, and technical validation.

The strategic task is therefore not only to create more programmes, but to connect existing assets into a continuous operational pipeline. Founders should be able to move from idea generation to incubation, technical validation, acceleration, financing, market entry, and scaling through a system that is easier to navigate and more consistent across regions and sectors.

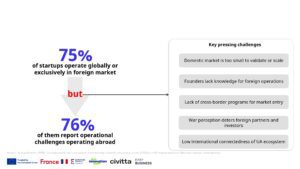

International ambition needs stronger market-access support

Ukrainian startups think globally by default. 75% of Ukrainian startups operate internationally or exclusively in foreign markets, a rational response to a small domestic market. This is a rational response to the limited size and depth of the domestic market, especially for high-growth technology companies. Yet 76% of Ukrainian startups operating abroad report operational difficulties abroad, from legal setup to customer acquisition.

Ukraine already has several market-access channels, including Diia.Business, the Entrepreneurship and Export Promotion Office, international delegations, startup events, matchmaking initiatives, ecosystem media, and bilateral bridge models such as the UK–Ukraine TechBridge.

Still, internationalisation support remains too episodic. Founders often need to navigate foreign-market entry largely on their own, relying on individual networks, ad hoc opportunities, or short-term programmes. The domestic market also remains underused as a source of early demand. Public procurement, in particular, does not yet function as a predictable route for startup validation and market creation, except in selected defence and dual-use areas.

The report recommends building a more structured market-access pipeline. This means stronger and more bridge programmes with priority foreign markets, better market-entry preparation, advisory vouchers, soft-landing support, grants for international expansion, and more systematic corporate-startup and public-sector pilot opportunities.

Five shifts needed for the next stage

The study identifies 74 recommendations, including 22 priority initiatives. Together, they point to five core shifts needed to strengthen Ukraine’s startup ecosystem.

- First, Ukraine needs to move from fragmented policy measures to a coherent startup-policy architecture. This requires shared legal definitions, clearer institutional ownership, stronger coordination, and a reliable startup data and monitoring system.

- Second, the financing system needs to move from fragmented grants and isolated investments to a continuous funding ladder. Public resources should be used to activate private capital, not replace it.

- Third, Ukraine needs to move from technical talent strength to startup-ready talent. This means strengthening entrepreneurship education, founder role models, university startup support, and skills development linked to priority innovation sectors.

- Fourth, support infrastructure needs to move from parallel initiatives to a connected pipeline. Early-stage support, sector-specific acceleration, university commercialisation, regional hubs, and prototyping infrastructure should work together more consistently.

- Fifth, international orientation needs to become a structured market-entry pathway. Ukrainian startups already think globally; the ecosystem now needs to provide stronger institutional support to help them enter, validate, and scale in foreign markets.

The full report is available for download below.

This publication was funded by the European Union, co-funded by the French Government, and supported by Expertise France within the EU4Innovation East project. Its contents are the sole responsibility of Civitta and EasyBusiness and do not necessarily reflect the views of the European Union, the French Government, or Expertise France.